Disintermediation and the Costs of Traditional Investing.

Disintermediation – is the process of cutting out an intermediary or middleman, typically to increase profits.

According to Wikipedia “The term was originally applied to the banking industry in about 1967: disintermediation referred to consumers investing directly in securities (government and private bonds, and stocks) rather than leaving their money in savings accounts, then later to borrowers going to the capital markets rather than to banks.(OED, Google News Archive) The original cause was a US government regulation (Regulation Q) which limited the interest rate paid on interest bearing accounts that were insured by FDIC.”

The second financial reference to the term was common among business school professors in the early 1990s. They were correctly referring to the trend for corporate borrowers to bypass the banks and look directly towards the capital markets as source of funds. The goal was not only lower financing costs but also eliminating or reducing potentially restrictive financial covenants imposed by the lender. Although most corporations still maintain bank credit facilities they typically serve as a backstop to commercial paper programs. The non-investment grade or middle market company is more likely to rely upon banks as a direct source of financing.

We may be approaching the third phase of financial disintermediation. This is envisioned as a phase whereby retail investors bypass the traditional advisor (and the recurring annual cost) allowing for a considerable improvement in realized return over the investment horizon. The same concept applies to the many talented portfolio managers and analysts. However the fact is that over the long-term apparently less than 20% of these actively managed funds beat the relevant index after expenses. If commissions are paid to enter or exit the fund the results may be considerably worse. The appropriate question seems to be are these parties consistently adding value? And if not is there a viable alternative? It seems probable that as investors become more educated they will pursue a strategy of disintermediation allowing for increased portfolio values over the long term. SunPillar is positioned to assist investors with this transition.

The Costs of Intermediation (“middleman”)

The costs vary widely depending on factors such as fund performance, fund operating expenses, and cost of investment advisor. Additionally a less obvious cost is the tax effect relating to higher portfolio turnover that takes place in actively managed funds. This turnover rate varies widely, but a figure of 80% or higher is not uncommon. Portfolio turnover affects taxes by forcing capital gains distributions to owners. The tax rate on these gains is dependent on how long the security was held: less than one year and the ordinary income tax likely applies; more than a year and the capital gains tax (15% for most individuals) would generally be applicable.

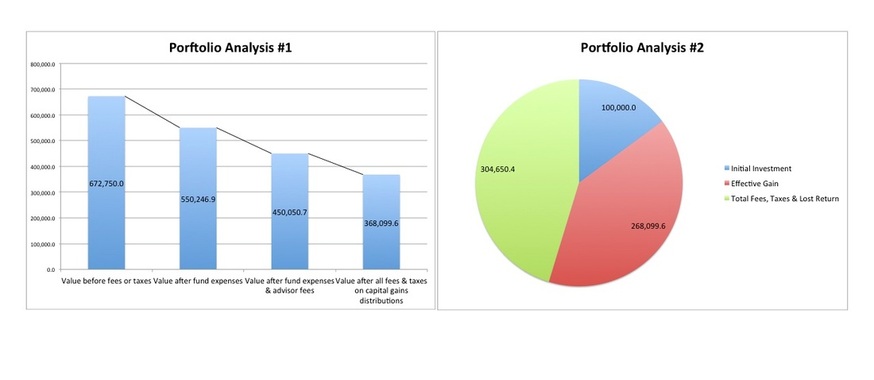

The charts below show the potential impact of fund operating costs, advisor costs and capital gains taxes on a single $100,000 investment yielding a 10% pre-cost pretax return over a 20-year period. The fund operating costs, financial advisor costs and capital gains tax are each assumed to be 1% per year. (These costs can vary significantly based on a number of factors including, but not limited to, fund management style, fund selection, portfolio turnover, size of portfolio and institution acting as advisor).

Under this $100,000 one time 20-year investment scenario the investor’s total gain is eclipsed by costs, fees, taxes & lost return totaling $304,650.4. Expressed differently total return without these costs/fees would have increased by an additional 113.6 % or $304,650.4 to a final portfolio value of $672,250 (instead of $368,099.6). This scenario did not include any potential additional costs associated with front end or back end loaded (commission) funds.

To be fair even investing in index funds or ETFs involves some costs – and these funds may also generate a small amount of capital gains due to necessary rebalancing and other factors. However, it is reasonable to believe that costs reduction of 80% or greater is easily achievable by investing directly in passively managed index funds, ETFs and/or securities.

A back of the envelope method to roughly estimate costs of investing can be accomplished by adding annual fund operating expense + investment adviser annual cost + expected annual reduction in return attributable to capital gains distribution (capital gains tax is the among the most difficult variables to estimate although there is some correlation with portfolio turnover). In the example above the total cost was approximately 3% per year – which may not sound very high. This translates to earning approximately 3% less per year than the equivalent market return. When this differential is compounded over time this example shows the impact can be dramatic. For equivalent investments of shorter duration the impact would be smaller. Also, the higher the percent market return, the larger the dollar difference in return and the smaller the percentage difference in return. It is important to note in our example that the lost return component – the return that would have otherwise been earned on funds that were withdrawn to pay fees and costs - is slightly larger than the “actual” hard dollar fees/costs/taxes.

(Notes: Specific timing of fee withdrawals during a year will have a marginal impact on overall costs. Additionally all taxable portfolios are subject to capital gains tax in effect at the time of liquidation. The capital gains tax in the scenario above relates solely to projected distributions made by the fund to owners attributable to portfolio turnover. Also the allocation of costs to advisor, fund or capital gains may change slightly based on the priority/order of payment. However, the total payments & lost return would be relatively unchanged as would the final portfolio value after fees and capital gains distribution taxes. The above analysis is not intended to address all costs associated with investing, but rather highlight the potentially significant difference in costs between Traditional Investing and Direct Investing. The SEC's website provides an in depth discussion of different costs associated with mutual fund investing http://www.sec.gov/answers/mffees.htm#distribution.

CONTACT US:

SunPillar Financial Advisors LLC

(p) 646-285-3493; (f) 917-522-9648

steve@sunpillarfinancialadvisors.com

(p) 646-285-3493; (f) 917-522-9648

steve@sunpillarfinancialadvisors.com